Hsmb Advisory Llc for Beginners

The Ultimate Guide To Hsmb Advisory Llc

Table of ContentsIndicators on Hsmb Advisory Llc You Need To KnowThe 7-Minute Rule for Hsmb Advisory LlcThe Only Guide to Hsmb Advisory LlcAbout Hsmb Advisory Llc4 Easy Facts About Hsmb Advisory Llc ExplainedRumored Buzz on Hsmb Advisory LlcHsmb Advisory Llc Things To Know Before You Get This

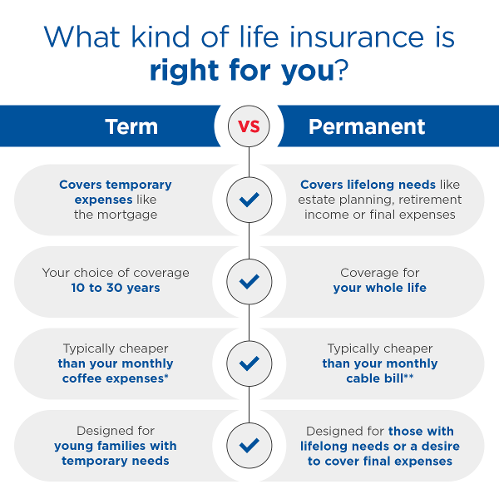

Be conscious that some policies can be expensive, and having certain wellness conditions when you apply can enhance the premiums you're asked to pay. You will require to ensure that you can pay for the premiums as you will certainly require to devote to making these settlements if you want your life cover to continue to be in positionIf you really feel life insurance coverage might be valuable for you, our partnership with LifeSearch permits you to get a quote from a number of providers in dual quick time. There are different sorts of life insurance that aim to fulfill different defense requirements, including level term, lowering term and joint life cover.

The Only Guide for Hsmb Advisory Llc

Life insurance policy provides five financial benefits for you and your family members (St Petersburg, FL Health Insurance). The major advantage of adding life insurance policy to your economic strategy is that if you die, your successors obtain a round figure, tax-free payment from the policy. They can use this money to pay your final expenditures and to change your revenue

Some plans pay if you create a chronic/terminal ailment and some supply financial savings you can make use of to sustain your retired life. In this write-up, discover about the various advantages of life insurance policy and why it may be a great idea to purchase it. Life insurance coverage supplies benefits while you're still active and when you die.

Some Ideas on Hsmb Advisory Llc You Should Know

If you have a policy (or plans) of that size, individuals that depend upon your income will certainly still have cash to cover their continuous living expenses. Recipients can make use of plan benefits to cover important day-to-day costs like rent or home mortgage payments, energy bills, and grocery stores. Average yearly expenditures for households in 2022 were $72,967, according to the Bureau of Labor Statistics.

Rumored Buzz on Hsmb Advisory Llc

Development is not affected by market problems, allowing the funds to accumulate at a steady rate with time. Additionally, the money worth of entire life insurance policy grows tax-deferred. This suggests there are no revenue taxes accumulated on the cash worth (or its development) until it is taken out. As the cash money value develops with time, you can use it to cover costs, such as getting an automobile or making a deposit on a home.

If you make a decision to obtain against your money worth, the finance is not subject to revenue tax as long as the plan is not surrendered. The insurer, nevertheless, will certainly charge rate of interest on the financing amount till you pay it back (https://www.quora.com/profile/Hunter-Black-120). Insurance provider have varying rate of interest prices on these car loans

The 45-Second Trick For Hsmb Advisory Llc

For instance, 8 out of 10 Millennials overestimated the cost of life insurance in a 2022 research. In reality, the typical price is more detailed to $200 a year. If you think buying life insurance may be a wise monetary action for you and your family, consider consulting with an economic expert to adopt it into your economic strategy.

The five primary types of life insurance policy are term life, whole life, universal life, variable life, and final expense insurance coverage, additionally called burial insurance. Each type has different attributes and advantages. For instance, term is extra inexpensive however has an expiration date. Entire life begins out costing much more, but can last your whole life if you maintain paying the premiums.

About Hsmb Advisory Llc

It can settle your financial obligations and clinical costs. Life insurance can also cover your mortgage and provide money for your family to maintain paying their bills. If you have household depending on your revenue, you likely need life insurance coverage to support them after you pass away. Stay-at-home moms and dads and company owners also usually need life insurance policy.

For the a lot of component, there are 2 sorts of life insurance policy intends - either term or irreversible strategies or some combination of the two. Life insurance providers use various types of term plans and standard life policies as well as "rate of interest sensitive" products which have actually become a lot more common because the 1980's.

Term insurance coverage supplies security for a given amount of time. This period could be as short as one year or give insurance coverage for a details variety of years such as 5, 10, 20 years or to a defined age such as 80 or in many cases up to the oldest age in the life insurance coverage mortality tables.

Facts About Hsmb Advisory Llc Uncovered

Presently term insurance coverage rates are very competitive and among the lowest traditionally experienced. It must be kept in mind that it is an extensively held idea that term insurance coverage is the least pricey pure life insurance policy coverage offered. One requires to copyrightine the plan terms carefully to decide which term life options are ideal to meet your certain situations.

With each brand-new term the costs is boosted. The right to Recommended Site renew the policy without proof of insurability is an important benefit to you. Otherwise, the danger you take is that your wellness may degrade and you might be unable to acquire a plan at the exact same prices and even whatsoever, leaving you and your beneficiaries without coverage.